Vegan Pet Food Market Size, Share

Report Overview

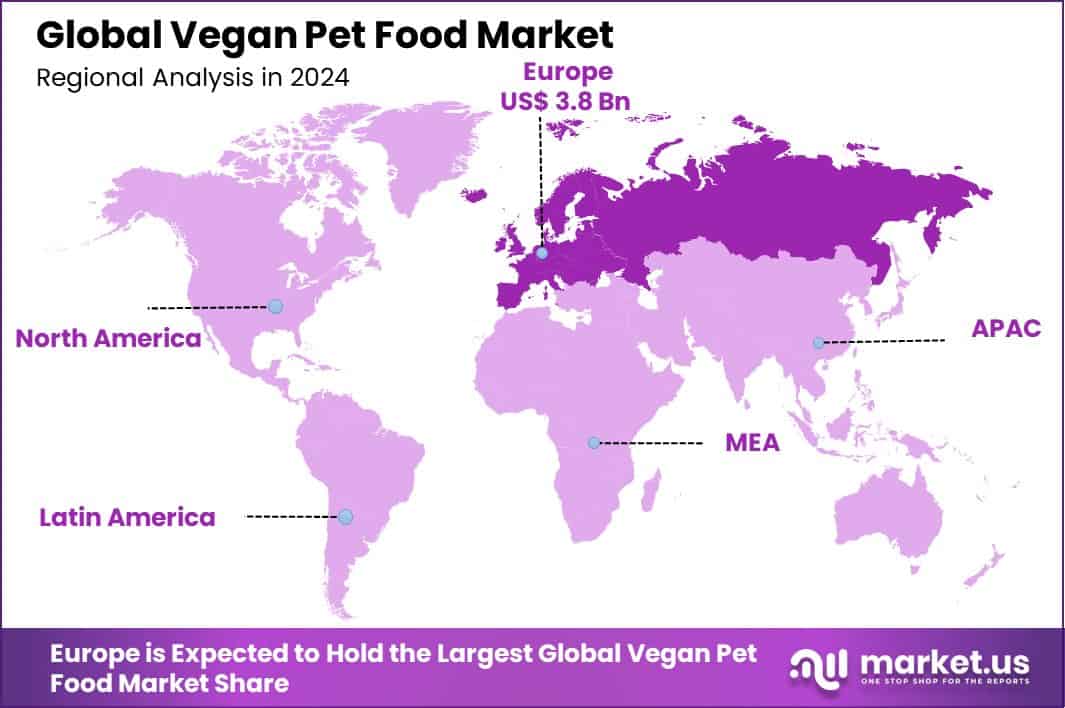

Global Vegan Pet Food Market is expected to be worth around USD 19.7 billion by 2034, up from USD 10.3 billion in 2024, and grow at a CAGR of 6.7% from 2025 to 2034. With a USD 3.8 billion valuation, Europe dominated the Vegan Pet Food Market, capturing a 36.90% share.

Vegan pet food is a plant-based alternative to traditional animal-derived pet diets, formulated to meet the nutritional needs of pets without using meat, dairy, or other animal byproducts. It includes ingredients such as legumes, grains, vegetables, and synthetic amino acids to ensure a balanced diet. Growing concerns about pet health, environmental sustainability, and ethical treatment of animals are driving the shift toward plant-based pet diets. As awareness of the carbon footprint associated with animal agriculture increases, more pet owners are seeking sustainable food options for their animals.

The vegan pet food market is expanding rapidly, fueled by rising consumer demand for ethical and environmentally friendly pet nutrition. The market is benefiting from significant investment in plant-based and alternative-protein pet food startups. In 2022, OMNI, a UK-based vegan pet food startup, raised €1.3 million to support its expansion. Similarly, Good Dog Food, a cultivated pet food manufacturer, secured £3.6 million ($4.5M/€4.1M) in seed funding in 2023, signaling investor confidence in alternative pet food solutions.

Consumer demand for vegan pet food is increasing as pet owners seek healthier, hypoallergenic, and sustainable dietary options. Many pets suffer from food allergies linked to traditional animal-based diets, making plant-based alternatives appealing. Munich-based Vegdog, which raised €3.5 million in Series A funding in 2021, has capitalized on this trend by offering nutritionally complete vegan dog food. The rise in veganism among pet owners has also influenced their purchasing decisions, further driving market growth.

Opportunities in the vegan pet food market are growing as innovative startups receive financial backing to scale production and distribution. Scrumbles, a UK startup offering plant-based dog food, received £6 million ($7.3 million) in funding from BGF in 2023. This trend reflects increasing investor confidence and consumer interest in alternative pet diets. Expanding product availability in mainstream retail channels and the development of plant-based pet treats and supplements present further growth opportunities for the sector.

Key Takeaways

- Global Vegan Pet Food Market is expected to be worth around USD 19.7 billion by 2034, up from USD 10.3 billion in 2024, and grow at a CAGR of 6.7% from 2025 to 2034.

- Conventional vegan pet food dominates with a 63.20% market share, reflecting consumer preference for familiar formulations globally.

- Dogs account for 72.30% of the vegan pet food market, indicating strong demand among canine owners worldwide.

- Dry pet food holds a 56.20% share, showcasing its convenience, longer shelf life, and ease of storage.

- Supermarkets and hypermarkets contribute 48.20% to distribution, highlighting consumer preference for accessible retail shopping experiences.

- Holding a 36.90% market share, Europe’s Vegan Pet Food Market was valued at USD 3.8 billion in 2024.

By Form Analysis

Conventional form holds a dominant 63.20% share globally.

In 2024, Conventional held a dominant market position in the By Form segment of the Vegan Pet Food Market, with a 63.20% share. Conventional vegan pet food remains the preferred choice among pet owners due to its affordability, availability, and established manufacturing processes.

Pet food brands continue to focus on expanding their conventional product lines, offering dry kibble, wet food, and treats with plant-based proteins such as peas, lentils, and soy. The market is witnessing increased investments in improving the nutritional profile of conventional vegan pet food to ensure essential nutrient sufficiency for pets.

The demand for vegan pet food is primarily driven by pet humanization trends, where owners seek healthier and ethical food options. Many consumers are shifting toward plant-based pet food due to concerns over food allergies, digestion issues, and obesity in pets. Additionally, growing awareness of sustainability and the environmental impact of meat-based pet food is accelerating the market growth. Consumers increasingly prefer vegan formulations that minimize carbon footprints while maintaining pet health.

Opportunities lie in product innovation, including enhanced taste and texture to improve pet acceptance. Manufacturers are focusing on partnerships with veterinarians and retailers to increase market reach, particularly in emerging economies where awareness is steadily growing.

By Pet Type Analysis

Dogs account for 72.30% of the total pet food consumption.

In 2024, Dog held a dominant market position in the By Pet Type segment of the Vegan Pet Food Market, with a 72.30% share. The high market share is attributed to the increasing number of pet owners opting for plant-based diets for their dogs due to health benefits, sustainability concerns, and ethical considerations.

Dogs, being omnivorous, can adapt more easily to vegan diets compared to cats, driving the demand for plant-based dog food formulations. Key players in the market are focusing on improving the protein quality and nutrient balance in vegan dog food to ensure complete and balanced nutrition.

The rising trend of pet humanization and increasing cases of food allergies among dogs are key demand drivers for vegan pet food. Many pet owners are switching to plant-based diets to address digestive issues, obesity, and skin allergies in their pets. The growing availability of fortified vegan dog food with essential nutrients such as taurine and omega fatty acids is further fueling market expansion.

Market opportunities lie in product innovation, expanded distribution networks, and veterinary endorsements. Companies investing in taste enhancement, bioavailability of plant-based nutrients, and premium vegan dog food options are expected to gain a competitive advantage in the evolving market landscape.

By Product Type Analysis

Dry pet food leads with 56.20% preference among pet owners.

In 2024, Dry Pet Food held a dominant market position in the By-Product Type segment of the Vegan Pet Food Market, with a 56.20% share. The segment’s strong performance is driven by the convenience, affordability, and longer shelf life of dry vegan pet food compared to wet and fresh alternatives.

Pet owners prefer dry kibble due to its ease of storage, portion control, and suitability for automated feeders. Additionally, manufacturers are focusing on improving the palatability and nutritional content of dry vegan pet food by incorporating plant-based proteins, fortified amino acids, and essential vitamins.

The rising trend of sustainable and health-conscious pet diets is accelerating the demand for dry vegan pet food. Pet owners are increasingly seeking plant-based formulations that reduce environmental impact while ensuring optimal nutrition. The segment benefits from wider retail availability, including supermarkets, pet specialty stores, and e-commerce platforms, further strengthening its market penetration.

Opportunities exist in formulation advancements, flavor enhancements, and premium dry vegan pet food offerings. Companies investing in novel ingredients such as insect-based protein and alternative plant-based sources are expected to gain a competitive edge. Expansion into emerging markets, along with veterinarian-recommended formulations, will further drive segment growth.

By Distribution Channel Analysis

Supermarkets and hypermarkets dominate distribution with a 48.20% market share.

In 2024, Supermarket/Hypermarket held a dominant market position in the By Distribution Channel segment of the Vegan Pet Food Market, with a 48.20% share. The segment’s strong foothold is driven by widespread accessibility, competitive pricing, and the ability for consumers to physically assess product quality before purchase.

Supermarkets and hypermarkets offer a broad selection of vegan pet food brands, allowing pet owners to compare ingredients, nutritional value, and pricing. The presence of dedicated pet food aisles and promotional discounts further strengthen consumer preference for this retail channel.

The rising demand for plant-based pet diets, coupled with increasing consumer awareness, has led supermarkets and hypermarkets to expand their vegan pet food offerings. Leading retailers are allocating more shelf space to sustainable and organic pet food products, reflecting growing market demand. The availability of private-label vegan pet food at competitive prices also contributes to the segment’s growth.

Opportunities exist in enhancing product visibility, in-store promotions, and strategic retail partnerships. Vegan pet food brands focusing on exclusive supermarket tie-ups and in-store education campaigns can further boost sales. Additionally, expansion into high-growth regions through supermarket chains is expected to drive market penetration and long-term segment expansion.

Key Market Segments

By Form

By Pet Type

By Product Type

- Dry Pet Food

- Wet Pet Food

- Treats and Snacks

- Others

By Distribution Channel

- Supermarket/Hypermarket

- Specialty Stores

- Online Sales Channel

- Others

Driving Factors

Growing Pet Humanization and Ethical Consumerism

Pet owners increasingly view their pets as family members, driving demand for healthier and ethically sourced food options. The shift toward pet humanization has led to a rise in demand for plant-based pet diets, aligning with human dietary preferences.

Many consumers are choosing vegan pet food due to concerns about factory farming, animal welfare, and the environmental impact of meat production. Ethical consumerism is pushing brands to offer sustainable, cruelty-free, and high-nutrient alternatives.

Additionally, younger pet owners, particularly millennials and Gen Z, are more likely to seek eco-friendly and ethical pet food options. As awareness grows and product availability increases, vegan pet food continues to gain traction, reshaping the traditional pet food market landscape.

Restraining Factors

Nutritional Concerns and Pet Health Uncertainty

One of the biggest challenges in the vegan pet food market is ensuring complete and balanced nutrition for pets, especially cats, which are obligate carnivores. Many pet owners worry that plant-based diets may lack essential nutrients like taurine, vitamin B12, and omega-3 fatty acids, which are naturally found in animal-based food.

While vegan pet food brands use fortified ingredients, skepticism remains regarding long-term health impacts. Veterinarians and pet nutritionists often caution against fully plant-based diets without proper supplementation.

Additionally, some pets may struggle with digestibility and acceptance of vegan formulations. These concerns create hesitation among consumers, slowing adoption rates. Overcoming this challenge requires continued research, improved formulations, and stronger veterinary endorsements to build trust in the market.

Growth Opportunity

Innovation in Plant-Based Protein and Supplements

The growing vegan pet food market presents a major opportunity for innovation in plant-based protein sources and nutrient-rich supplements. Companies are developing high-quality, bioavailable plant proteins such as pea, lentil, and quinoa to improve the nutritional profile of vegan pet food.

Additionally, advancements in synthetic amino acids, omega-3 alternatives like algae oil, and fortified vitamin blends help address concerns about essential nutrient deficiencies. Improved formulations can enhance pet health, digestion, and acceptance of plant-based diets.

As research progresses, brands that invest in better taste, texture, and complete nutrition solutions will gain a competitive edge. Collaborations with veterinarians and pet nutritionists can further strengthen consumer confidence, driving long-term growth in this evolving market.

Latest Trends

Rise of Premium and Organic Vegan Pet Food

A key trend in the vegan pet food market is the increasing demand for premium and organic formulations. Pet owners are becoming more conscious about ingredient quality, preferring non-GMO, organic, and minimally processed plant-based food for their pets.

Brands are responding by launching high-protein, grain-free, and allergen-free options that cater to specific dietary needs. Superfoods like quinoa, chia seeds, and algae-based omega-3 are being incorporated to enhance nutritional value.

Additionally, freeze-dried and air-dried vegan pet food is gaining popularity as a nutrient-dense alternative to traditional dry kibble. With pet humanization on the rise, consumers are willing to pay more for high-quality, ethically sourced, and vet-approved vegan pet food, fueling the premiumization trend in this market.

Regional Analysis

In 2024, Europe led the Vegan Pet Food Market with a 36.90% share, reaching USD 3.8 billion.

In 2024, Europe dominated the Vegan Pet Food Market with a 36.90% share, valued at USD 3.8 billion. The region’s strong market presence is driven by high pet ownership rates, growing veganism, and stringent regulations favoring sustainable pet food alternatives. The increasing number of pet parents opting for plant-based diets due to ethical and environmental concerns has accelerated market growth. The presence of key manufacturers and an expanding retail network further support market expansion.

North America follows closely, witnessing strong demand for vegan pet food due to rising pet humanization and health-conscious consumers. The U.S. and Canada are leading markets, with increasing product availability in supermarkets and e-commerce platforms.

Asia-Pacific is emerging as a high-growth region, driven by increasing awareness and rising disposable incomes in countries like China, Japan, and Australia. However, market penetration remains lower compared to Western regions.

The Middle East & Africa,a and Latin America are in the early adoption phase, with growing urbanization and pet ownership trends contributing to demand. Increasing investments in premium pet food and expanding retail distribution are expected to support growth. As awareness rises globally, vegan pet food brands continue expanding into these developing markets.

Key Regions and Countries

- North America

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global vegan pet food market in 2024 is witnessing strong competition among key players as demand for sustainable and ethical pet diets rises. Companies are focusing on product innovation, expanding distribution networks, and strengthening brand positioning to capture market share.

Ami Planet Srl continues to hold a strong presence in Europe, leveraging its premium, nutritionally complete vegan pet food offerings. The company benefits from growing consumer preference for organic and high-quality plant-based pet food. Expanding into new retail and e-commerce channels remains a strategic focus.

Antos B.V. is actively enhancing its product portfolio with vegan pet treats and chews, catering to the rising demand for healthy, natural alternatives. Its dominance in the European pet food sector provides a strong foundation for future growth.

Anything Vegan Private Limited is capitalizing on Asia-Pacific’s emerging vegan pet food market, targeting consumers seeking affordable, plant-based alternatives. Product diversification and improved nutritional formulations will be critical for its market expansion.

Benevo has built a strong reputation in the cruelty-free pet food segment, offering fortified vegan diets for both dogs and cats. Its veterinarian-approved formulations and certifications give it a competitive advantage in Europe and North America.

Bond Pet Foods, Inc. is leading the way in alternative protein innovation, using fermentation-based, meat-free pet food solutions. This biotech-driven approach is set to redefine the plant-based pet food industry.

Compassion Circle, Inc. remains a niche player, focusing on specialized vegan pet diets. Strategic expansion and branding will be key to increasing its global market presence.

Top Key Players in the Market

- Ami Planet Srl

- Antos B.V.

- Anything Vegan Private Limited

- Benevo

- Bond Pet Foods, Inc.

- Compassion Circle, Inc.

- FreshWoof – Urban Tails Pvt. Ltd.

- Halo Pets

- Isoropimene Zootrofe Georgios Tsappis Ltd.

- My Aistra

- Soopa Pets

- THE PACK PET LIMITED

- V-dog, Inc.

- Vegeco Ltd.

- Wild Earth Inc.

- YARRAH

Recent Developments

- In February 2025, we collaborated with Meatly to launch Chick Bites in the UK—the world’s first cultivated chicken dog treats, sold at Pets at Home.

- In 2024, THE PACK PET LIMITED FreshWoof Urban Tails Pvt. Ltd. expanded distribution in India and announced plans to enter international markets (Australia, Singapore, UK) by 2025. Launched plant-based “Power Meals” with Ayurvedic ingredients.

Report Scope

link